June update: financial and tax policy changes in China

June 8, 2021

Brighture, one of our key firms in China, has published its latest newsletter for June 2021.

It discusses the latest updates regarding financial and tax policy changes in China.

June 8, 2021

Brighture, one of our key firms in China, has published its latest newsletter for June 2021.

It discusses the latest updates regarding financial and tax policy changes in China.

June 7, 2021

Pass through cost – whether mark up to be added? Perspective of tax authorities in India

By Amit Ajmera, Kreston SGCO, India

In the recent round of a Transfer Pricing Assessment (“TPA”) of an Indian entity, a Wholly-Owned Subsidiary (“WOS”) of a foreign entity, the transfer pricing authorities in India have taken a view that the pass-through cost billed by the WOS to its parent entity and reimbursed by the parent entity to the WOS, should be done with a mark-up and not on the cost to cost basis. The said cost needs to be included in the marked-up cost base for determining the arms-length arrangement between the WOS and its group entity.

Background

The taxpayer is part of a multinational group that is in the business of undertaking clinical trial activities globally. To undertake the said business activities, typically one of the entities in the group (i.e., the service provider) would enter into a service agreement (i.e., a Master Service Agreement or “MSA”) with a pharmaceutical company (i.e., the service recipient or client) to undertake clinical trials in identified geographies. The agreement, among other things, categorically states that the pass-through cost incurred by the service provider while providing the services will be reimbursed by the service recipient on a cost-to-cost basis. Which expense would qualify as the pass-through cost is also defined in the said agreements. Further, the agreements clarify that the pass-through cost that would be incurred in any part of the identified geographies will have to be recovered only by the entity entering into the MSA with the service recipient and not by another group entity, which may be undertaking clinical trials in its respective geography. Pass through cost are cost which are required to be incurred during undertaking clinical trials that are required to be paid by the pharmaceutical company to the sites (hospitals), investigators (doctors) and patients. But because it is administratively not possible, the pass-through cost is normally paid by the service provider and recovered from the service recipient.

Facts of our client

In the case of the Indian WOS, on the basis the MSA entered into by its group entity with its client, the group entity had entered into a service agreement with the WOS in India. In addition, there was also a tripartite agreement that was entered into among the WOS, the site, and the investigators in India for undertaking clinical trial activities in India. The service recipient, in this case, had also signed the agreement as a confirming party to the agreement entered among the Indian Parties. The medicines / drugs that were required for undertaking the clinical trials in India were supplied directly by the service recipient to the site. To undertake the clinical trials, the Indian entity had to make payments to the sites and the investigators which were like pass-through cost. The same was invoiced by the WOS to the group entity on the cost to cost basis. This was in addition to the invoice raised by the WOS on the group entity for the services of clinical trials rendered by it. The invoice for intercompany services was raised on a cost-plus basis.

View of the transfer pricing authorities at a lower level

The transfer pricing officer has taken a position that the pass-through cost should be added to the marked-up cost base for determining whether the transaction between the WOS and the group entity is on an arm’s length basis.

Way forward

We have filed an appeal with the higher authority challenging the view of the lower level.

June 1, 2021

Transfer Pricing in the STA 2021 General Tax Control Plan

By Mario Quiliez, Mario Pires & Elena Ramirez

The 2021 publication of the Annual Tax and Customs Control Plan in early February has confirmed that the Spanish Tax Agency is looking more and more closely, in their investigations and checks for tax fraud, at issues associated with related-party transactions and transfer pricing in multi-national groups, large corporations, and medium-sized companies.

The special economic and financial conditions due to the coronavirus pandemic and the State’s response to its effects pose significant challenges for both companies and tax administrations, from a practical standpoint, in applying the arm’s length principle.

The Spanish Tax Agency, to tackle challenges from 2021 and in studies regarding transfer pricing for 2020 (the year of the outbreak and spread of Covid-19) and following years, will take into account the guidelines recently passed for the Inclusive Framework on BEPS on the application of the Organisation for Economic Co-operation and Development (“OECD”) transfer pricing guidelines, concerning several specific issues arising from or exacerbated by the Covid-19 pandemic, as well as their consistency with the general pricing policy of companies or business groups.

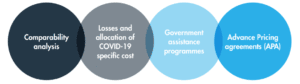

Specifically, the issues covered in the recent OECD guidelines, as a practical example of how the arm’s length principle should be applied to related-party transactions impacted by the Covid-19 crisis, are as follows: (i) comparability analysis; (ii) losses and the allocation of Covid-19 specific costs; (iii) government assistance programmes; and (iv) advance pricing agreements (“APAs”).

Furthermore, for 2021, STA has announced a specific campaign to verify proper compliance with obligations to report related-party transactions on form 232. It is important to note that the information reported on this form must be consistent with the transfer-pricing dossier. Likewise, failure to report operations and/or reporting inaccurate data on the 232 form is a serious tax violation, punishable with a fine of up to 2% of the value of the operations not reported or inaccurately reported.

Other priority focuses announced, regarding related-party transactions, are:

All the above confirms that Spanish companies with related-party transactions must properly document transfer pricing, which must be in line with the company’s transfer pricing policy, taking into account that studies from 2020, and for other years affected by the situation caused by the coronavirus, the OECD Guidance on the transfer pricing implications of the Covid-19 pandemic will apply.

As a final note, in recent years, the Spanish Tax Agency has been looking closely at issues related to transfer pricing and related-party transactions, as per guidance from the OECD.

May 26, 2021

Stanley & Williamson rebrands to adopt Kreston name

One of our Australian member firms, Stanley & Williamson, has completed its rebrand and adoption of the Kreston name.

We are delighted that they shall now be known as Kreston Stanley Williamson.

May 21, 2021

Kreston Global Tax Group’s webinar on the impact of Brexit on international tax structuring, held on 12 May 2021, gathered over 45 tax specialists within our Network.

The webinar focused on the impact of Brexit on tax regulations and trade across the UK, US, European and Asian markets.

Special thanks to Mark Taylor, Leader of Kreston Global Tax Group, and to all our panellists Don Reiser, Ganesh Ramaswamy, Guillermo Narvaez, Jelle Bakker, Sharon Bedford for sharing their local perspective.

Kreston members can view the event page for more information and related resources.

May 19, 2021

Losses in a limited-risk entity pursuant to the OECD Guidance on the Transfer Pricing Implications of the Covid-19 Pandemic

By Guillermo Narvaez, Tax Partner at Kreston FLS Mexico

The OECD guidance on the transfer pricing implications of the Covid-19 pandemic (referred to as the “Guidance”) was issued in December 2020. The idea was to give light to taxpayers and tax administrations on what to do about intercompany operations and how to apply the methodology of transfer pricing determined in the OECD TP Guidelines (“OECD TPG”) due to ‘fact patterns that may arise commonly in connection with the pandemic’.

There is a permanent discussion in transfer pricing related to ‘limited risk’ distribution operations and how to deal with this kind of transaction. A point to stress is whether a limited-risk distribution business could afford losses or these businesses are not ‘entitled’ to generate them.

There is neither a rule in the OECD TPG nor the Guidance related to losses generated by limited-risk distribution operations. Moreover, the term ‘limited risk’ is not defined in the OECD TPG. However, what is expected is that distributors with low risks have profits regularly and if losses are generated these should be part of an isolated fact not frequently repeated; however, this is only convention. When a subsidiary has full support from its related parties to make the distribution of products with moderate risks, the least expected thing is to deal with risks that could finally drive operating losses.

The fact is that a limited-risk operation can indeed generate losses, and this matter should not be a concern for the taxpayer nor the tax authority as long as the risks associated with the distribution operation and borne by the distributor, including the financial risk, are assumed by the latter.

If the terms of the agreement between related parties were those that independent businesses would have agreed and the negative operating result of the distribution operation is directly coming from applying such terms, the loss will probably make sense. Note that risks during a pandemic may be exacerbated. Nonetheless, the contractual terms should not be necessarily modified because of force majeure.

The Guidance is clear when it states that ‘It is important to emphasize that in the absence of clear evidence that independent parties in comparable circumstances would have revised their existing agreements or commercial relations, the modification of existing intercompany arrangements and/or the commercial relationships of associated parties is not consistent with the arm’s-length principle’.

Each case should be analysed to understand the background and effect of the pandemic on the specific operation accurately to get conclusions on what to do when a loss is incurred by a low-risk distribution operation.

Another matter is that the pandemic does not suffice to change the transfer pricing method applied in previous years. The Guidance is clear with regard to fostering the OECD TPG aims without modifying the arm’s length principle and its rules, all of them determined in the OECD TPG.

The Guidance is focused on giving light on what is needed to do in an extraordinary event like the pandemic suffered since the beginning of 2020 but in some cases with a very general view.

May 18, 2021

TP-Link is a global provider of reliable networking and wi-fi devices and accessories, distributing to more than 170 countries and serving billions of people worldwide. Its products include ‘smart’ bulbs, plugs and cameras for people’s homes and cloud solutions, routers and high-speed wired and wireless networking for businesses.

TP-Link UK’s group auditor is Kreston Reeves, led by Peter Manser. During 2020, the company carried out a restructure. This meant that TP-Link NL needed a group audit to reflect the new corporate structure and Kreston Reeves referred the company to Van Herwijnen Kreston (VHK). After a short proposal process, TP-Link NL appointed VHK as its group auditor. They are also advising on income tax assessment, general tax matters and our Dutch firm Bentacera is assisting in transfer pricing support and documentation.

This successful outcome demonstrates the strength and reach of the Kreston International network. It also shows how the network can help smooth the changes many companies have to make following the UK’s departure from the EU.

Olivier Walravens, from Van Herwijnen Kreston, said “We were pleased to be able to help TP-Link change its group audit process so effectively and efficiently. Sharing and transferring the necessary data and documents was straightforward as Kreston firms are part of the same, secure system.”

Chris Sun, International Accountant at TP-Link NL, said: “We’re very grateful to Kreston for making this major change so ‘smart’. It was achieved in good time and they took care of everything for us. Using firms within the Kreston network has undoubtedly saved the company time and money.”

May 14, 2021

Practical application of the arm’s length principle in the context of the Covid-19 pandemic

By Carlos D’Arrigo, Transfer Pricing and Valuation Partner, Kreston BDM

In 2021 most taxpayers around the world would face an unprecedented challenge to reflect how their 2020 transactions compared to fair and open market values simply because in a crisis downturn like no other with disruptions and restrictions across almost every industry, how can you define what market conditions were fair? In the so-called phrase “business as usual”, how can you explain “usual”? We are not quite certain either but let’s try to find some answers.

On December 18, 2020, the 137 members of the Organization for Economic Co-operation and Development (“OECD”) Inclusive Framework on Base Erosion and Profit Shifting Action Plan (“BEPS”) released the Guidance on the transfer pricing implications of the COVID-19 pandemic (the “Guidance”) with the purpose of helping both taxpayers and tax administrations in reporting the financial periods affected by the pandemic in compliance with the arm’s length principle[1]. The guidance provides insights for the following four priority issues:

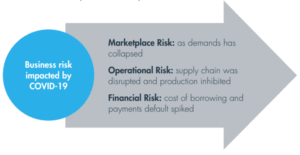

The Guidance recommends to first identify each specific cause that impacted taxpayers results and group them into three risk bubbles: Market Risk, Operational Risk and Financial Risk. The following chart intends to show a more comprehensive process flow:

Identify specific cause

• Drop in sales volume and/or price

• Increase in material and labour cost

• Increase in overhead expenses

• Exceptional, non-recurring, extraordinary operational cost

• Decrease in capacity utilisation or economy of scale

• Increase in days inventory and obsolescence

• Increase in days Receivable

• Increase in interest rates and bank fee charges

Once specific causes are identified, the Guidance suggests addressing each of them on a case by case basis using the following sources of contemporaneous information to support the performance of a comparability analysis applicable for Fiscal 2020:

Guidance suggested source |

Our comments |

| Pre-COVID sales vs. 2020 actual | Be mindful when using new product/services data that could distort comparability, also marketing strategies to retain customers |

| Pre-COVID utilization vs 2020 actual | Economies of scales, cost structures and operating leverage, break-even analysis |

| Exceptional, non-recurring, extraordinary operational cost | Warehousing, logistics, overtime, transport, insurance |

| Government grants, subsidies, programs | Employee retention cost, rental and lease cost, tax waivers, deferral of contributions, interest |

| Macroeconomic data | GDP by country, sector or region, and trade association data can be helpful to confirm Pre-COVID sales vs. 2020 actual conclusions. Macroeconomics analyses might use data such as market share variation and drop in consumption, demand and other market metrics |

| Regressions | Regression analysis of variance analysis is more reliable to

predict variations when a large amount of data inputs are included; thus, it might be of limited help. |

| 2020 Budget vs 2020 real | Budget data is unlikely to be considered official data for controversy or court cases. |

Finally, Guidance made important remarks about comparability adjustments that are likely to be rejected by tax administrations including the following:

Guidance remarks |

Our comments |

| Prior global crisis comparison | Since COVID-19 is an unprecedented crisis like no other, using data from other global crisis, such as the 2008/2009 financial crisis, could lead to poor and superficial conclusions |

| Using Loss-making comparables | Although the Arm’s Length principle does not override the inclusion or exclusion of loss-making comparables[2] as long their inclusion/exclusion satisfy the comparability criteria, extra care should be taken when performing comparability analysis for fiscal 2020 ensuring that chosen comparables assumed similar levels of risk and that have been similarly impacted by the pandemic. |

| Intercompany renegotiations | Related parties that renegotiated certain terms in their existing agreements are advised to identify clear evidence that independent parties in comparable circumstances would have revised their existing agreements or commercial relations, otherwise, such modification of existing intercompany arrangements and/or the commercial relationships of associated parties is deemed to be considered not consistent with the arm’s length principle. Examples of fair renegotiation might include: renegotiate a contract to support the financial survival of any of the transactional counterparties, or to retain key customers, |

| Limited-risk arrangements | Consistency is key to support changes in limited-risk arrangements, for instance, a “limited-risk” distributor did not assume any marketplace risk Pre-COVID and hence was only entitled to a low return, but in 2020 argues that the same distributor assumes some marketplace risk and hence should be allocated losses, is expected to keep bearing such risk in 2021 and so on. |

| Force majeure adjustments | Taxpayers should carefully review existing intercompany arrangements when invoking a force majeure clause to ensure that: i) the arrangement actually includes a written force majeure clause, ii) if no clause existed but one was added in 2020, such clause is also expected to remain in force after the pandemic, iii) the law governing the contract is not a civil law jurisdiction where force majeure would automatically apply, and iv) the specific related party situation actually qualifies as a force majeure. |

As discussed above, reporting the financial periods affected by the pandemic in compliance with the arm’s length principle cannot be done with one single and straightforward approach, in this particular challenge, our preferred approach is to build up from a pre-COVID vs. 2020 actual comparability analysis which in fact compares the actual tested party with itself as long as the pre-COVID pricing policy was not intended to aggressively shift profits within the MNE.

[1] The foundation of transfer pricing is the arm’s length principle, which states that the price, terms and conditions charged in a controlled transaction between two related parties should be the same as that in a transaction between two unrelated parties on the open market. In other words, an arm’s length transaction refers to a business deal in which buyers and sellers act independently without one party influencing the other.

[2] It worth noting that in many cases, domestic legislation and/or tax administration ruling prescribe against the use of loss-making comparable.

May 13, 2021

Our Chinese firm, Brighture, has recently published its latest newsletter discussing recent tax changes for businesses and private individuals.

The newsletter covers new financial and tax policies, service cases, Brighture salon, Kreston updates, and their business structure.

May 12, 2021

Q&A: Liza Robbins on commerce, people and the future of accounting

Our CEO, Liza Robbins, has recently taken part in a Q&A session with AccountancyAge in which she discusses and gives insight into her work at Kreston and how she sees the future of accounting.

By Guillermo Narvaez – Technical Director of the Kreston International Global Tax Group

Digital Services Taxes (DSTs) are a new global initiative designed to charge larger technology companies that provide digital platforms such as social media, advertising, online marketplaces and other search engine tools for commercial transactions or selling user data online advertising. It is beginning to apply across the world at the behest of the G20 – the Organisation for Economic Co-operation and Development (OECD) who are calling for changes to the international tax system to address the challenges of the digitisation of the economy by mid-2021.

A simple enough idea – impose additional tax costs on those who earn more – but is it really this simple? Who actually pays this tax, as on the face of it, it is the customers themselves who face liability rather than the platforms on which they are advertising.

Online platforms essential for SMEs to grow

Big tech companies like Amazon, Google and Apple shift the tax burden instigated by DSTs downstream to their customers, many of whom are SMEs. The European Centre for International Political Economy (ECIPE) has stated that “the EU’s commercial landscape is characterised by an overall share of highly diverse SMEs who account for 99.8% of all EU enterprises and 66.6% of overall EU employment.”

Copenhagen Economics also point out that 82% of SMEs in Europe use search engines to promote products and services online, while 42% of SMEs use online marketplaces to sell their products and services.

So we can see that SMEs are disproportionately affected by DSTs and are the ones left with the bill.

But in reality, to what extent are DSTs targeting the big fish? The DSTs’ purpose is well-meaning – challenge some of the world’s largest multinational enterprises (MNEs) to pay their dues.

However, when these enterprises can just pass this on to others – particularly digitally dependent SMEs who cannot otherwise achieve their goals – the DST is surely not having its desired effect?

Not looking at the profitability of the platforms means that the DST may end up being a disproportionate levy and, as a result, drive a possible deceleration of economic growth.

SMEs are inadvertent “victims” of the new tax levy

So what is the thinking behind this new levy? Many SMEs exist either in the middle of the digital services supply chain or to ensure the delivery of a product or service to its final customer. Where tech companies at one end of the chain and final customers at the other, SMEs sit between the two, paying for services (such as advertising) provided by the tech companies.

The logic of the DST is, in part, that tax on profitability (such as income tax) do not have the reach to impose tax burdens on tech companies for digital services. However, tech companies can circumvent the economic burden of the DST by transferring the levy to their customers, as they currently do with SMEs.

Conversely, whilst tech companies can pass on the levy to SMEs by increasing the cost of their services and so cover their tax liability, SMEs cannot similarly shift the burden downstream to their customers, as doing so may well take away their competitive advantage.

A well-meaning but flawed tax concept

Finally, even though consumers successfully use one or more digital service, they do not usually have to pay anything at all. Most of these can access any information, products and services through the use of free online services.

While SMEs serve a vital purpose in domestic economies, they are often the primary victims of this tax burden, whereas tech companies escape cost-free. Hence this system of taxation is a flawed one and deeply unfair.

SMEs are part of the digital services supply chain and a vital element of any country seeking to pursue economic growth while achieving a healthy economy. Since over 99% of EU businesses are SMEs, surely it would be fairer to support their development, rather than leave them to have to shoulder most of the actual tax burden?

(a version of this article also appeared in Accountancy Daily, May 12th 2021)

May 6, 2021

This publication aims to provide an overview of the different tax systems across Latin America, Spain and Portugal, to support member firms in this vital area of every practice.

Produced by Kreston Guatemala, other Kreston member firms in Latin America and Kreston Iberaudit, based in Spain.

May 3, 2021

Our Mexican firm, Kreston BSG, has provided a comprehensive publication on important aspects to consider in the subcontracting reform in Mexico that became law last month.

The publication explains the reform should be considered a legal system that establishes the conditions to enact new rules in using the subcontracting labour figure.

April 26, 2021

Balluff is an international, family-run business specialising in sensors and automation for sectors including assembly and logistics plants. It was founded 100 years ago near Stuttgart, Germany, and has since expanded into 68 countries.

Kreston Global has worked closely with Balluff for many years, helping it develop as a global player built on solid financial foundations.

We are involved in the decision-making process at all stages, advising on everything from company formations to large acquisitions. We audit the consolidated financial statements and all German subsidiaries and look after tax matters globally.

From our side, the relationship has been led by Michael Kalmbach for the last 20 years. He said: “We are really proud to have been involved in the development of Balluff – their development is a real success story. Our dedicated team contributes their business and tax know-how to make sure we always deliver solutions that overcome obstacles, often before they arrive.”

In addition to our ongoing audit and tax consulting advice, our focus is to help Balluff grow.. Our consolidated, scaleable processes have helped them implement transfer pricing solutions to make the business work efficiently across its global footprint.

Balluff is part of a growing industry where its customers are constantly seeking to increase efficiencies and reduce costs. “Kreston Bansbach are looking forward to helping Balluff do the same”, said Michael, “we are looking forward to working alongside them in their future development. Happy 100th Anniversary!”.

April 19, 2021

AUMA has been developing and building electric actuators and valve gearboxes for over 50 years. It supplies a wide range of industries including water, power, oil & gas and general industry.

As a global organization, with 2,600 employees and over 40 entites worldwide, AUMA is facing a growing complexity regarding financial and tax compliance, changes to existing business models as well as mergers & acquisitions. In order to keep pace with these challenges AUMA was searching for a reliable partner who is able to support its development and to deliver high quality and efficient services on a global stage.

For this reason, AUMA relies on the global network from Kreston Bansbach.

“We wanted to deliver more efficient co-ordination of the group audit and the consolidated financial statements as soon as possible,” said Eike Neumann, the Kreston Bansbach lead partner. “In addition, we enhanced managing AUMA’s international consulting project and teams.”

As a result, we also work together on other consultancy-intensive projects such as international transactions, international and complex transfer pricing, expansion projects as well as assisting the establishment of new AUMA companies and cross-company reorganisation projects.

Our expert team carries out complex and detailed work, such as financial, tax and legal due diligence in the context of transaction projects. We delivered on time, on budget and within all required legal deadlines.

“It was the right decision to engage Kreston as our trusted consulting company for numerous complex national and international projects. Especially the global coverage and presence of the Kreston network has proved to be a real value and key enabler for the success of our projects”, said Christoph Neubauer, Group Director Finance & Controlling.

April 8, 2021

Our Chinese firm, Brighture, has provided a comprehensive newsletter on recent tax changes for businesses and private individuals.

The newsletter covers new financial and tax policies, service cases, Brighture salon, Kreston updates, and their business structure.

March 31, 2021

Our Mozambique firm, Kreston Mozambique, has been busy using the Kreston network to its advantage with many new client successes.

Kreston Mozambique recently won a very successful three-year contract by utilising the Kreston network leveraging off the international network and working with two other Kreston firms based in Uganda and Myanmar.

They also won a proposal for a business valuation project working with Kreston South Africa to complete the work together. The client was “extremely happy with the high standard of professional relations and services that Kreston provided.”

We pride ourselves on the quality of work that all our Kreston members around the world deliver.

March 10, 2021

Our Chinese firm Brighture has provided a comprehensive article on recent tax changes for businesses and private individuals.

Please download their latest Newsletter here.

February 1, 2021

GUILLERMO NARVAEZ

International Tax Technical Director of the Kreston International Tax SIG

Kreston FLS, Mexico

For many decades, international tax (INTAX) advisory has been a key feature of the most important business-focused service firms. In many countries, this service was initially provided by accounting firms before extending to legal firms too. Why is it relevant to large international law/ accounting firms to advise on INTAX? In my view, the reason lies in the following points:

• INTAX is highly specialised. And INTAX is becoming ever more complex.

• INTAX is a subject always related to multinational companies (MNE). This is obviously due to operations being carried out or with effects in more than one jurisdiction.

• INTAX means competitiveness among jurisdictions; different states will compete to win foreign investment, which will generate wealth in their territories.

Competitiveness between states expands the possibilities of the MNEs to distribute their activity among multiple jurisdictions with the purpose of achieving greater fiscal efficiency. The freedom of choice to decide where a business is going to do certain activities contributes to forecasting the net global tax rate an MNE may pay. This is, in a nutshell, an exclusive attribute of the jurisdictions identified as ‘sovereignty’.

Accordingly, the jurisdictions create an offer for the MNEs to carry out tax strategies using various elements such as royalty and interest payments, hybrid operations, permanent establishments, strategies related to capital gains, or complicated corporate structures in several jurisdictions with attractive low or nil tax impact, among many other elements to assess.

As if these were not enough, in 2015 the OECD1 launched the BEPS2 project, trying to stop the shifting of profits to jurisdictions where no value was generated to the taxable activities. This generated a straight and quite clear implication – an urgent need for MNEs and companies doing international operations to be advised to efficiently face the new reality in INTAX.

Kreston’s INTAX experts and global collaboration has advantages over many other organisations; with more than 200 firms located in 110 countries, we cover the main economies of the world in areas where MNEs perform a large part of their operations.

There is a tendency to assume that only the large accounting firms (Big Four) or law firms are able to provide INTAX services. Yet good advice on international tax is provided by specialists who collaborate with other firms, regardless of company size.

Kreston’s INTAX experts and global collaboration has advantages over many other organisations; with more than 200 firms located in 110 countries, we cover the main economies of the world in areas where MNEs perform a large part of their operations.

January 28, 2021

ANDREW WALLIS

Corporate and International Tax Partner

Kreston Reeves, United Kingdom

The UK has consistently ranked as one of the best places to locate a holding company due to its robust legal system, relative political and economic stability, geographic location, time zone, language, low costs of company administration and attractive tax environment.

Given Brexit, however, should companies be looking elsewhere – such as Ireland or the Netherlands – to locate their holding companies? In short, although both Ireland and the Netherlands have their attractions and will of course remain within the EU, we do not think that the attractiveness of the UK will be greatly diminished by Brexit.

A whole range of tax issues should be considered when determining the best location for a holding company. Although the final decision will depend on a group’s unique circumstances and priorities, key considerations include the factors outlined below, which continue to position the UK as an attractive holding company location regardless of its non-EU status.

Corporate income tax rate

The UK has the lowest corporate tax rate of the G7 group of countries: 19%. The fact that this is not as low as Ireland’s 12.5% tax rate for trading income may not matter, given that most holding companies will not have significant business activities.

Withholding taxes

One of the most attractive features of the UK is that it does not impose withholding tax on the payment of dividends by a company. This means that profits can be returned to parent entities/shareholders with no tax leakage.

The UK also has the most extensive double tax treaty network in the world; the rate of withholding on payments of interest and royalties is often reduced from the non-treaty rate of 20%, or can even be exempt. Further, as the UK seeks to agree free trade deals with non-EU territories, there is the potential for term treaties to become even more generous and widespread.

Taxation of dividend income

Dividends and distributions received by UK companies are typically exempt from corporate income tax regardless of whether they are paid by UK or overseas companies. In particular, subject to specific anti-avoidance cases, the following are exempt:

Taxation on sale of subsidiaries

The ‘substantial shareholding exemption’ (SSE) exempts any capital gain on the disposal of shares in a subsidiary (UK or overseas) in cases where:

Though Ireland has its own version of SSE and the Netherlands has a participation exemption, the generosity of the UK’s SSE should not be overlooked.

Controlled foreign company rules

Like many jurisdictions, the UK has controlled foreign company rules. However, the UK has moved to a much more territorial basis of taxation that can mitigate the application of the CFC rules by offering a broad range of exemptions and exceptions. These include a tax avoidance gateway test, an excluded territories exemption, a low profits exemption and a low profit margin exemption.

Of course, both Ireland and the Netherlands have now incorporated controlled foreign company rules into their domestic legislation under the EU Anti-Tax Avoidance Directive.

Capital taxes

The UK does not impose capital taxes (stamp duty) on the issue of shares by a UK company, although most transfers of shares in a UK company are subject to stamp duty at 0.5%.