This guidelines provide a general view regarding the Venezuelan Value Added Tax (VAT) system. They focus on how it affects foreign entrepreneurships who trade with Venezuela. They are general and will very unlikely cover the singularities of your case. They must be read as such general guidelines and must not be interpreted as professional advice. Should you need professional advice on how VAT affects your entrepreneurship, please contact a VAT specialist of Kreston Venezuela.

Venezuela

September 12, 2023

Global vacancies

Municipio Chacao

July 8, 2021

News

Venezuela

July 2, 2021

Global vacancies

Brito, D’Arrigo, Martínez Kreston

June 10, 2021

News

Practical Application of the Arm’s Length Principle in the Context of the COVID-19 Pandemic

May 14, 2021

Practical application of the arm’s length principle in the context of the Covid-19 pandemic

By Carlos D’Arrigo, Transfer Pricing and Valuation Partner, Kreston BDM

In 2021 most taxpayers around the world would face an unprecedented challenge to reflect how their 2020 transactions compared to fair and open market values simply because in a crisis downturn like no other with disruptions and restrictions across almost every industry, how can you define what market conditions were fair? In the so-called phrase “business as usual”, how can you explain “usual”? We are not quite certain either but let’s try to find some answers.

On December 18, 2020, the 137 members of the Organization for Economic Co-operation and Development (“OECD”) Inclusive Framework on Base Erosion and Profit Shifting Action Plan (“BEPS”) released the Guidance on the transfer pricing implications of the COVID-19 pandemic (the “Guidance”) with the purpose of helping both taxpayers and tax administrations in reporting the financial periods affected by the pandemic in compliance with the arm’s length principle[1]. The guidance provides insights for the following four priority issues:

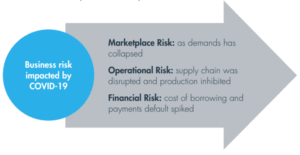

The Guidance recommends to first identify each specific cause that impacted taxpayers results and group them into three risk bubbles: Market Risk, Operational Risk and Financial Risk. The following chart intends to show a more comprehensive process flow:

Identify specific cause

• Drop in sales volume and/or price

• Increase in material and labour cost

• Increase in overhead expenses

• Exceptional, non-recurring, extraordinary operational cost

• Decrease in capacity utilisation or economy of scale

• Increase in days inventory and obsolescence

• Increase in days Receivable

• Increase in interest rates and bank fee charges

Once specific causes are identified, the Guidance suggests addressing each of them on a case by case basis using the following sources of contemporaneous information to support the performance of a comparability analysis applicable for Fiscal 2020:

Guidance suggested source

Our comments

Pre-COVID sales vs. 2020 actual

Be mindful when using new product/services data that could distort comparability, also marketing strategies to retain customers

Pre-COVID utilization vs 2020 actual

Economies of scales, cost structures and operating leverage, break-even analysis

Employee retention cost, rental and lease cost, tax waivers, deferral of contributions, interest

Macroeconomic data

GDP by country, sector or region, and trade association data can be helpful to confirm Pre-COVID sales vs. 2020 actual conclusions. Macroeconomics analyses might use data such as market share variation and drop in consumption, demand and other market metrics

Regressions

Regression analysis of variance analysis is more reliable to

predict variations when a large amount of data inputs are included; thus, it might be of limited help.

2020 Budget vs 2020 real

Budget data is unlikely to be considered official data for controversy or court cases.

Finally, Guidance made important remarks about comparability adjustments that are likely to be rejected by tax administrations including the following:

Guidance remarks

Our comments

Prior global crisis comparison

Since COVID-19 is an unprecedented crisis like no other, using data from other global crisis, such as the 2008/2009 financial crisis, could lead to poor and superficial conclusions

Using Loss-making comparables

Although the Arm’s Length principle does not override the inclusion or exclusion of loss-making comparables[2] as long their inclusion/exclusion satisfy the comparability criteria, extra care should be taken when performing comparability analysis for fiscal 2020 ensuring that chosen comparables assumed similar levels of risk and that have been similarly impacted by the pandemic.

Intercompany renegotiations

Related parties that renegotiated certain terms in their existing agreements are advised to identify clear evidence that independent parties in comparable circumstances would have revised their existing agreements or commercial relations, otherwise, such modification of existing intercompany arrangements and/or the commercial relationships of associated parties is deemed to be considered not consistent with the arm’s length principle. Examples of fair renegotiation might include: renegotiate a contract to support the financial survival of any of the transactional counterparties, or to retain key customers,

Limited-risk arrangements

Consistency is key to support changes in limited-risk arrangements, for instance, a “limited-risk” distributor did not assume any marketplace risk Pre-COVID and hence was only entitled to a low return, but in 2020 argues that the same distributor assumes some marketplace risk and hence should be allocated losses, is expected to keep bearing such risk in 2021 and so on.

Force majeure adjustments

Taxpayers should carefully review existing intercompany arrangements when invoking a force majeure clause to ensure that: i) the arrangement actually includes a written force majeure clause, ii) if no clause existed but one was added in 2020, such clause is also expected to remain in force after the pandemic, iii) the law governing the contract is not a civil law jurisdiction where force majeure would automatically apply, and iv) the specific related party situation actually qualifies as a force majeure.

As discussed above, reporting the financial periods affected by the pandemic in compliance with the arm’s length principle cannot be done with one single and straightforward approach, in this particular challenge, our preferred approach is to build up from a pre-COVID vs. 2020 actual comparability analysis which in fact compares the actual tested party with itself as long as the pre-COVID pricing policy was not intended to aggressively shift profits within the MNE.

[1] The foundation of transfer pricing is the arm’s length principle, which states that the price, terms and conditions charged in a controlled transaction between two related parties should be the same as that in a transaction between two unrelated parties on the open market. In other words, an arm’s length transaction refers to a business deal in which buyers and sellers act independently without one party influencing the other.

[2] It worth noting that in many cases, domestic legislation and/or tax administration ruling prescribe against the use of loss-making comparable.

Search

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to change your consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-advertisement

1 year

Set by the GDPR Cookie Consent plugin, this cookie is used to record the user consent for the cookies in the "Advertisement" category .

cookielawinfo-checkbox-analytics

11 months

This cookie is set by the GDPR Cookie Consent plugin. It is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

This cookie is set by the GDPR Cookie Consent plugin to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by the GDPR Cookie Consent plugin. It is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by the GDPR Cookie Consent plugin. It is used to store the user consent for the cookies in the category "Other".

cookielawinfo-checkbox-performance

11 months

This cookie is set by the GDPR Cookie Consent plugin. It is used to store the user consent for the cookies in the category "Performance".

CookieLawInfoConsent

1 year

Records the default button state of the corresponding category & the status of CCPA. It works only in coordination with the primary cookie.

device_id

10 years

Cookie used to maintain a local copy of the user's unique identifier.

viewed_cookie_policy

11 months

This cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not a user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Cookie

Duration

Description

__cf_bm

30 minutes

This cookie, set by Cloudflare, is used to support Cloudflare Bot Management.

bcookie

1 year

LinkedIn sets this cookie from LinkedIn share buttons and ad tags to recognize browser ID.

bscookie

1 year

LinkedIn sets this cookie to store performed actions on the website.

currency

1 year

This cookie is used to store the currency preference of the user.

lang

session

LinkedIn sets this cookie to remember a user's language setting.

li_gc

6 months

Linkedin set this cookie for storing visitor's consent regarding using cookies for non-essential purposes.

lidc

1 day

LinkedIn sets the lidc cookie to facilitate data center selection.

UserMatchHistory

1 month

LinkedIn sets this cookie for LinkedIn Ads ID syncing.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Cookie

Duration

Description

ac_enable_tracking

1 month

This cookie is set by Active Campaign to denote that traffic is enabled for the website.

device_view

1 month

This cookie is used for storing the visitor device display inorder to serve them with most suitable layout.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Cookie

Duration

Description

__kla_id

2 years

Cookie set to track when someone clicks through a Klaviyo email to a website.

_ga

2 years

This cookie is installed by Google Analytics. It is used to calculate visitor, session and campaign data and it also keeps track of site usage for the site's analytics report. The cookie stores information anonymously and assigns a randomly generated number to identify unique visitors.

_ga_M0XVMQMRZ1

2 years

This cookie is installed by Google Analytics.

_gat_gtag_UA_188891991_1

1 minute

This cookie is set by Google and is used to distinguish users.

_gat_gtag_UA_7661078_5

1 minute

This cookie is set by Google and is used to distinguish users.

_gid

1 day

This cookie is installed by Google Analytics. It is used to store information on how visitors use a website and helps to create an analytics report on how the website is performing. The data collected includes the number of visitors, the source of visitors and the pages visited in an anonymous form.

AnalyticsSyncHistory

1 month

Linkedin set this cookie to store information about the time a sync took place with the lms_analytics cookie.

CONSENT

16 years 5 months 19 days 16 hours 12 minutes

These cookies are set via embedded YouTube videos. They register anonymous statistical data e.g. how many times the video is displayed and what settings are used for playback. No sensitive data is collected unless you log in to your Google account, in that case your choices are linked with your account, for example if you click “like” on a video.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.