Nepal

May 1, 2026

May 1, 2026

April 2, 2026

Read the latest financial news and updates in China from experts at Kreston Brighture.

March 31, 2026

March 24, 2026

The Australian Research and Development (R&D) Tax Incentive is a Federal Government program designed to encourage companies to invest in innovation. It provides tax offsets for eligible R&D activities, helping reduce the cost of developing new products, processes, or technologies. There are two distinct steps requiring claimants to deal with two separate regulators: Industry Innovation and Science Australia and the Australian Tax Office.

March 13, 2026

APAC region tax Q1 tax update:

On 17 February 2026, the Full Federal Court held in Commissioner of Taxation v S.N.A Group Pty Ltd [2026] FCAFC 10 that payments made to associated enterprises were not deductible because the license agreements were not legally enforceable contracts. The court stressed that payments between related entities will not be deductible unless the taxpayer can demonstrate, through objective evidence, a real, enforceable obligation to pay, supported by objective evidence of agreement and consistent conduct. The decision reinforces those informal arrangements, even if standard within a business group, require clear documentation to support tax deductibility, as “arm’s-length” pricing alone does not prove a contract exists.

China has extended preferential tax treatments for Chinese Depository Receipts (CDRs) and for innovative enterprises till December 31, 2027, including exemptions on income tax for individual investors and for institutional investors. Individual investors are exempt from income tax on CDR disposals, with differentiated tax rates on dividends. Institutional investors, including qualified foreign institutional investors (QFIIs) and Renminbi qualified foreign institutional investors (RQFIIs), are exempt from enterprise income tax and value-added tax (VAT) on CDR disposals and related gains. The Chinese policy is extended to foster capital market investment in specific, high-growth, innovative industries. These incentives reduce the tax burden which results in an increase of trading volumes and attracts foreign capital.

Starting January 1, 2026, internet platform owners in Kazakhstan must submit monthly reports through the Integrated Tax Administration System (ITAS) regarding payments to resident sellers and service providers. Reports have to be filed by the fifth of the following month, requiring accurate, signed data on transactions and also with “nil” reports for inactive periods. Owners must disclose information on payments made to individuals, individual entrepreneurs, and legal entities residing in Kazakhstan. Reports must be submitted monthly, no later than the fifth day of the month following the reporting period.

In December 2025, the Singapore Government implemented the Multinational Enterprise (Minimum Tax) (Administrative Matters) Regulations 2025, detailing administrative rules for Singapore’s multinational enterprise top-up tax (MTT) and domestic top-up tax (DTT) regimes. The regulations outline qualifying conditions for designated filing entities, prescribed reporting events, record-keeping periods, and interest rules. If the €750 million threshold is met for at least two of the four fiscal years preceding January 1, 2025, registration must occur within 30 days of January 1, 2025. Companies that shifted tax residency from Singapore to a foreign jurisdiction after November 30, 2021, must also be disclosed.

The key amendments include :

March 12, 2026

Japan and the United Arab Emirates are converging into a powerful investment corridor. For investors in Dubai and multinational groups across the Gulf Cooperation Council (GCC), Japan has re-emerged as one of the most compelling destinations for long-term growth.

Japan’s GDP in 2025 is forecast to grow around 1.1%, supported by moderate inflation consistently above 2%, a sign of healthy demand and policy stability. Corporate earnings have strengthened, and capital markets have seen broad-based optimism over the past three years.

Tokyo has become one of the world’s most powerful economic cities, while Japan’s industrial strategy emphasises long-term investment in sectors such as semiconductors, green energy, AI, automation, robotics, and digital infrastructure and data centres.

The UAE and Japan share a long history of economic cooperation, but 2024–2025 brought a noticeable increase in two-way investment. For over 18 years, Kreston ProWorks has served as a full-service inbound advisory firm for foreign-owned companies in Japan. As members of Kreston Global, we work seamlessly with our colleagues in Dubai and Singapore to establish necessary relationships and build international structures that are strategically and fiscally optimised while remaining fully compliant in Japan.

We predict the next decade will be defined by stronger Asia–Middle East connectivity. Japan’s focus on technological resilience, industrial independence, and sustainability aligns closely with the UAE’s ambitions to become a global nexus for capital, innovation, and logistics.

With the right structure, advisory team, and local partner, Japan becomes not just a market to enter, but a strategic base for global expansion. At Kreston ProWorks Japan, we stand ready to support investors on this journey and to strengthen the bridge between Dubai and Tokyo for years to come.

![]()

Indonesia capital market reforms are being considered after the January 2026 MSCI crisis exposed weaknesses in ownership transparency and investor disclosure, triggering a catastrophic 7.35% IHSG collapse. This revealed a systemic disconnect, while UBO disclosure regulations existed through Presidential Regulation 13/2018, Indonesian accounting standards (PSAK) inadequately reflected these requirements, enabling complex ownership structures that frustrated international investors. The government is looking at major reforms to restore investor confidence.

For Indonesia’s accounting profession, this crisis presents unprecedented opportunities in corporate restructuring advisory, UBO mapping services, and specialised training on ownership-transparency analytics. However, firms face formidable challenges: developing new verification methodologies for complex conglomerate structures, accepting expanded professional liability, and working within compressed timelines to prevent Indonesia’s catastrophic downgrade to Frontier Market status by May 2026. Success requires transforming PSAK from standards permitting opacity to those demanding transparency, positioning Indonesia as a regional leader in beneficial ownership disclosure.

The crypto asset industry’s oversight in Indonesia also underwent a significant change in January 2025, affecting the operational legitimacy of local crypto exchange platforms. The Financial Services Authority (OJK) is now the current regulator of crypto assets following the formal transfer of authority from the Commodity Futures Trading Regulatory Agency (Bappebti). The transition represents a structural shift from a commodity-based regulatory approach toward integration within the financial service supervisory framework. Bank Indonesia continues to retain authority over payment system and monetary aspects.

Kreston Indonesia expects that this transition will lead to the issuance of clear and uniform accounting guidelines. Currently, our firm serves several crypto audit clients with engagements led by our audit partners, Mr. Leknor Joni and Mr. Ronady Sembiring.

From an audit perspective, crypto assets constitute a significant risk. Our auditors are applying a risk-based approach, and we are closely monitoring further regulatory developments and updates issued by the OJK and Bank Indonesia to ensure compliance with the applicable provisions across our crypto audit engagements.

India has surpassed Japan to become the world’s fourth-largest economy, highlighting the country’s strong growth momentum and rising influence in the global economic landscape.

Real GDP grew by 8.2% in Q2 FY 2025–26, the fastest rate among major economies. The International Monetary Fund (IMF) projects growth of 6.2% in 2026, while Goldman Sachs forecasts a stronger 6.9%, supported by resilient domestic consumption, relatively low inflation averaging 2.2% in 2025, and interest rate cuts of 125 basis points by the Reserve Bank of India.

With this momentum, India is widely expected to continue climbing the global economic rankings. Current projections suggest the country could become the world’s third largest economy by 2030, with GDP estimated to reach approximately USD 7.3 trillion.

Foreign direct investment (FDI) continues to play a significant role in India’s economic expansion. In FY 2024–25, inflows reached a record USD 81.04 billion, representing a 14% year-on-year increase and pushing cumulative FDI since 2000 beyond the USD 1 trillion milestone.

These inflows reflect investor confidence in India’s long-term growth potential, supported by structural reforms, a large domestic market and expanding digital infrastructure.

India has also emerged as the global hub for Global Capability Centres (GCCs). More than 2,100 GCCs now operate across the country, contributing approximately USD 64 billion to the economy and employing over two million professionals.

These centres increasingly support high-value functions including research and development, data analytics, technology services and financial operations, reinforcing India’s role within global corporate networks.

The investment outlook received an additional boost with the announcement of a landmark EU–India Free Trade Agreement in January 2026. The agreement is expected to eliminate tariffs on more than 90% of traded goods, strengthening trade flows and deepening economic ties between India and Europe.

For international businesses, the agreement is likely to improve market access and supply chain integration between the two economies, while supporting investment in sectors such as manufacturing, technology and services.

Taken together, strong domestic demand, expanding technology capabilities and sustained foreign investment suggest India’s economic rise will remain a defining feature of the global economy in the coming decade.

Kreston Global firms in India are among the network’s largest presences worldwide, with more than 20 offices and around 450 professionals across the country, reflecting the scale and growing importance of the Indian market within the global business landscape.

![]()

March 11, 2026

Foreign direct investment (FDI) surges in Thailand, with a significant increase in 2025 and overall investment hitting the THB 1.36 trillion, a 66% increase from 2024. International investors accounted for 72% of all BOI-promoted projects, totalling THB 1.88 trillion in pledged investment.

Board of Investment (BOI) data showed that by project count, machinery and automotive led with 487 projects (20%), followed by electrical appliances and electronics with 447 projects (18%), and metals and materials with 424 projects (18%).

By investment value, the digital sector dominated with THB 625.8 billion (46%), followed by electrical appliances and electronics at THB 271.3 billion (20%), and metals and materials at THB 145.5 billion (11%). China, Singapore, Hong Kong, Taiwan, Japan, and the Netherlands lead BOI investment flows, drawn by Thailand’s strategic location, competitive costs, BOI incentives, and skilled workforce.

These trends highlight Thailand’s continued appeal as a regional investment destination. With strong manufacturing capabilities, a rapidly expanding digital sector and sustained policy support from the Board of Investment, the country is well positioned to attract further foreign direct investment in the years ahead.

Kreston Thailand helps international businesses through comprehensive market-entry consulting, entity setup, and ongoing compliance management. Working with our global network, we deliver cross-border solutions, from company setup and ongoing compliance matters to APAC-wide M&A opportunities.

![]()

The Singapore budget introduces new measures to boost liquidity, including expanded startup funding, investment support and tax incentives designed to strengthen the country’s capital markets.

Singapore is allocating S$1bn to strengthen StartUp SG Equity, a government co-investment programme, in a bid to foster innovative, locally grown technology startups. These measures highlight how the Singapore budget aims to boost liquidity while supporting the next generation of high-growth companies.

Another S$1.5bn, continuing the Anchor Fund Scheme introduced in 2025, will be invested in high-growth companies to strengthen Singapore’s exchange market. An additional S$1.5bn will also be allocated to asset managers, ultimately boosting Singapore’s overall liquidity and investor attractiveness.

Additionally, it was announced in the Budget that grant support for small and medium-sized enterprises (SMEs) will be raised to 70% and 50% for non-SMEs of eligible costs incurred for overseas market promotion, business development, and market setup.

Singapore businesses will also benefit from a 40% corporate income tax rebate for 2026 alongside enhanced support for global expansion under the Double Tax Deduction for Internationalisation Scheme. This enables businesses to claim up to S$400,000 in tax deductions on expenses related to market research and studies for investment exploration or expansion outside Singapore.

For multinational companies, the new domestic top-up tax will be raised to 15% from FY2027, following the BEPS 2.0 (Pillar Two) global minimum tax framework. This ensures profits generated in Singapore are taxed in line with evolving global standards.

The introduction of Philippines 99-year land leases marks a landmark reform aimed at strengthening the country’s appeal to foreign investors. This, coupled with reduced income tax rates and streamlined duties, underscores the government’s commitment to creating a highly competitive and business-friendly environment.

The Government has also updated the Public-Private Partnership (PPP) law, which streamlines processes, enhances transparency, and de-risks infrastructure projects, thereby inviting greater private-sector participation in nation-building.

Beyond policy, the Philippines continues to solidify its position as a global hub for Business Process Outsourcing (BPO)and Global Capability Centers (GCCs). The sector demonstrates robust growth, expanding beyond traditional voice services to encompass high-value functions such as IT, finance and accounting, and creative services.

The country’s young, skilled, and English-proficient workforce, combined with ongoing digital infrastructure enhancements, ensures the Philippines remains a top choice for companies seeking scalable and efficient global operations. These developments collectively signal a dynamic and opportunistic landscape for network partners.

February 4, 2026

Rocel Magtibay, Human Resource Director, Kreston Helmi Talib, Singapore:

As a member of the Kreston Global network, we place significant value on building strong, collaborative relationships with fellow member firms. Secondments create opportunities for deeper operational alignment, shared learning, and stronger professional connections that benefit both our firm and the wider network. In addition, we view international assignments as an important component of developing future managers and leaders. Exposure to different audit environments, client expectations, and cultural contexts accelerates professional growth. Approving these secondments enables us to offer high-potential employees a developmental pathway that enhances both their technical expertise and their global mindset.

The partnership and coordination between SW Accountants and Advisors and our firm, Kreston Helmi Talib, have been collaborative and seamless throughout the entire secondment process. Following the standard selection procedure, we provided SW with a candidate profile aligned to their requirements for an Audit Senior. With the support of Hannah from SW’s HR team, as well as their audit leadership, the evaluation and selection process progressed smoothly and efficiently. From the issuance of the offer letter to visa processing and eventual onboarding, the communication flow remained clear, timely, and well-coordinated. Both firms maintained a thoughtful and proactive approach, ensuring that all administrative, compliance, and logistical matters were handled promptly. This partnership contributed to a positive experience for the secondee and an efficient overall transition.

For this secondment, we set clear expectations with the secondee ahead of her placement to ensure she was prepared for the transition. Although the secondment period from August to October coincides with a slower period for our Audit team in Singapore, we were informed that SW Accountants & Advisors would be in the midst of their peak season. We communicated this upfront, helping her anticipate the volume, pace, and level of client demands she would experience upon joining the SW team. We also emphasised the developmental value she would gain through this opportunity, including exposure to different audit methodologies and software, working within a new team structure, and operating in a different professional and cultural environment. These experiences were positioned as key growth drivers that would broaden her technical capabilities and strengthen her adaptability.

Keshika returned from the secondment motivated and inspired, despite the relatively short duration of the assignment. She valued the hands-on exposure she gained in a new environment and shared insightful reflections on how she adapted to different audit approaches, team dynamics, and work culture. The experience strengthened her confidence, broadened her technical and professional perspective, and enhanced her ability to manage change effectively.

Keshika Ravichandran, Audit Senior, Kreston Helmi Talib, Singapore

I felt that participating in a secondment within the Kreston Global network would allow me to gain broader professional exposure, including exposure to different clientele and industries. It would also allow me to deepen both my technical skills and personal growth.

My role during the secondment differed from my responsibilities at my home firm. In my home firm, engagements are usually handled by the audit-in-charge from acceptance to completion of an audit, together with the manager and partner-in-charge. During the secondment, my role was more focused on specific accounts and areas of the audit, with an overall more collaborative approach alongside the rest of the engagement team.

The experience exposed me to different industries which I had not encountered before and strengthened both my technical skills and resilience, as I had to familiarise myself with new software, tools and methodology in an unfamiliar environment. Working with new and diverse colleagues, including different leadership styles, allowed me to grow my relationship-building and collaboration skills. Through this secondment, I also gained insight into best practices such as audit documentation and risk assessment, which I can apply in future engagements at my home firm.

Adapting to a different work culture and expectations was a challenge at the start. I also had to navigate new software, tools, methodology, local FRS, auditing standards and SOPs on the job, while managing personal adjustments to housing, lifestyle and routine, alongside feeling homesick. During my first week, I completed the essential training and looked up resources to familiarise myself with the firm’s SOPs. Although it was a challenge to balance independence with asking for help, my colleagues at the secondment firm were kind, welcoming and supportive, which allowed me to adjust quickly. My family, friends and colleagues from my home firm also checked in on me often, which helped me overcome feeling homesick.

Overall, the secondment allowed me to grow both professionally and personally. It has driven me to challenge myself, particularly in improving my documentation and exercising professional judgement. Following the secondment, I communicated my desire to be assigned to more complex clients to my team lead.

Kreston Global secondments are just one of the ways the network brings together our people and supports international training and development.

October 30, 2025

Read the latest financial news and updates in China from experts at Kreston Brighture.

October 13, 2025

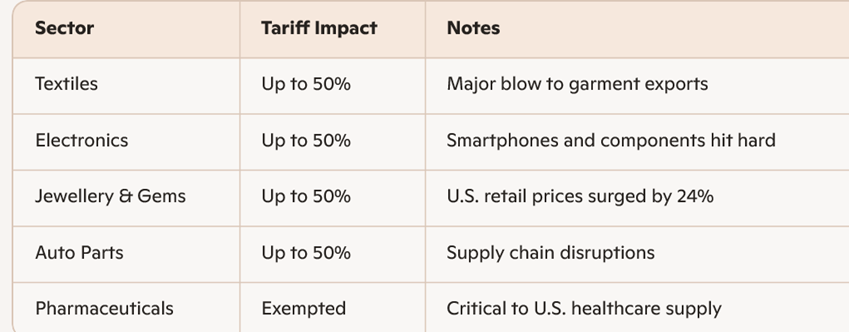

In 2025, US tariffs and the Indian economy hit the headlines, with the U.S.–India trade relationship facing its most dramatic rupture in decades. President Donald Trump’s sweeping tariffs — reaching up to 50% on Indian goods — and a sharp hike in H-1B visa fees sent shockwaves across industries. While headlines focused on textiles, electronics, and auto parts, the deeper story lies in how India’s service sector, especially IT, is responding.

And it’s not just about survival. It’s about transformation.

The tariffs disproportionately affected consumer and industrial exports:

India’s IT giants — TCS, Infosys, Wipro, HCL Tech — saw mixed earnings, margin pressures, and client hesitation. Mid-tier firms like Coforge and Persistent Systems, however, outperformed by staying agile and niche-focused.

While the tariffs directly target goods, the services sector—especially IT and business process outsourcing (BPO)—is feeling indirect pressure:

Despite these risks, India’s diversified service export base and strong digital infrastructure offer some insulation. However, analysts caution that prolonged tensions could erode India’s competitive edge in global services.

While the Trump administration’s tariff escalation poses serious challenges, it also opens up strategic opportunities for India to rethink its trade, technology, and diplomatic playbook

India’s resilience lies in its ability to adapt, innovate, and lead. This moment, though turbulent, could be the inflection point for a more self-reliant and globally diversified India.

The U.S. tariff escalation may feel like a setback, but it’s also a wake-up call—a chance for Indian businesses to evolve beyond traditional dependencies and embrace a more resilient, globally agile future. By diversifying markets, investing in innovation, and strengthening digital capabilities, companies can not only weather this storm but also emerge stronger, smarter, and more self-reliant.

This isn’t just damage control—it’s a pivot toward long-term transformation. The world is watching. And it’s India’s moment to rise and redefine the future.

September 22, 2025

August 11, 2025

Kreston Cambodia has written a summary of the key takeaways of Cambodia’s new Transfer Pricing procedures for 2025.

The Cambodian General Department of Taxation (GDT) has introduced updated transfer pricing (TP) rules through Prakas 574, dated 19 September 2024, to take effect in 2025. The new framework aligns more closely with OECD guidelines and expands the definition of a “related party” to include any entity that directly or indirectly controls, is controlled by, or is under common control with the taxpayer. This includes the relationship between a permanent establishment and its non-resident parent.

“Control” is defined as holding at least 20% of equity interest or voting rights in a company’s board of directors. However, the GDT retains discretion to determine control based on the facts of each case.

The rules mandate that all Cambodian entities engaging in related-party transactions prepare and maintain Local File TP documentation annually. Transactions covered include loans, sales and purchases of goods, leases, royalties, transfers of intangible assets, and technical or management service fees.

Cambodia’s approach adopts the arm’s length principle and recognises OECD-standard TP methods such as Comparable Uncontrolled Price (CUP), Resale Price Method (RPM), and Transactional Net Margin Method (TNMM). While there is no Mutual Agreement Procedure (MAP) in place, disputes can be addressed through the GDT’s local audit mechanism.

Kreston Cambodia’s TP team supports businesses with compliance, including preparing Local File documentation and benchmarking studies; audit defence strategies; audit support leveraging local and international expertise; strategic planning to optimise supply chains and related-party transactions; and tailored advisory services to ensure both compliance and tax efficiency.

Kreston Cambodia is part of the global Kreston network, providing audit, tax, accounting, and advisory services in Phnom Penh and beyond.

For more information, contact Kreston Cambodia at www.krestoncambodia.com.

July 18, 2025

In 2025, the China-US trade relationship—one of the most significant bilateral economic ties globally—underwent substantial turbulence. Tariff policies emerged as a central instrument in the strategic rivalry between the two nations. Over the year, these policies transitioned from a phase of intense confrontation to a period of temporary easing, marked by a series of rapid and substantial adjustments. The frequency and magnitude of these changes represent a rare chapter in global trade history.

A review of China’s official announcements throughout 2025 highlights the escalation and subsequent de-escalation of tariff measures imposed in response to US actions.

Further progress was made in June during negotiations held in London, building on the Geneva Agreement. Two major outcomes emerged:

While these developments provided temporary relief for Chinese enterprises, fundamental disagreements persist. The US maintains a 20% tariff on fentanyl and continues to apply a 10% base tariff across the board. Meanwhile, China upholds restrictions on rare earth element exports. Underlying technological competition between the two countries also remains unresolved.

The ongoing tariff conflict, marked by both escalation and partial resolution, has had far-reaching effects on Chinese businesses. These effects vary by industry and company size and have influenced areas ranging from financial performance to operational strategy. Key impacts include:

1. Export challenges and operational strain

2. Supply chain realignments

3. Heightened uncertainty and compliance burdens

The China-US tariff fluctuations in 2025 posed serious challenges for Chinese enterprises, but they also acted as a catalyst for growth and adaptation. Businesses responded with innovation, supply chain transformation, and market diversification—strategies that will serve them well in an unpredictable global trade landscape.

Looking ahead, it is vital for both China and the US to enhance communication and cooperation. By doing so, they can promote a stable and mutually beneficial trade relationship and contribute to broader global economic prosperity and order.

July 3, 2025

The sixth, and final edition of Going Global is now available, spotlighting the mid-market outlook in Africa.

This edition explores how geopolitical shifts, regional reforms, and emerging investment priorities are shaping opportunities for mid-sized businesses across the African region.

Download the latest magazine here.

Kreston Global has offices in over half of Africa and ranks as the 10th largest network in the region. Its Africa network includes 27 firms employing over 1,500 professionals across more than 27 countries. In 2025, the network is set to grow further through strategic additions and expansions in key markets across the continent.

Africa features nine of the top 20 fastest-growing economies, driving strong demand for accounting services, notably in Nigeria where Kreston Pedabo has achieved nearly 70% growth in two years. Angola has also attracted significant investment, inspiring expansion from Mozambique-based Kreston expert Dev Pydannah. In Ethiopia, TAY Audit Service LLP is focusing on youth development, recognising that 70% of the population is under 30.

We explore these themes and more in this edition. You can download the full magazine or browse the individual articles online here:

Follow us on social media

Find more updates on our LinkedIn page here.

June 19, 2025